PieDAO: Aligning Incentives in DeFi

PieDAO: Aligning Incentives in DeFi

Incentive alignment is the most significant prerequisite for productivity. To that end, PieDAO is an index-focused project trailblazing a revolution in DeFi governance structures

Implicit in the first line of Satoshi’s White Paper (“Commerce on the Internet has come to rely almost exclusively on financial institutions serving as trusted third parties…”) is the inference that trusting in third-parties encourages competition between the aforementioned, thus resulting in a “zero-sum” game focused solely on the redistribution of resources along the lines of the Pareto distribution. The predator-prey dynamics of such a society are, to a greater or lesser extent, an inevitability within any human society, and for a society to disentangle itself entirely from such animalistic tendencies as described in the Hobbesian theory of the “state of nature” is a near impossibility due to the incentives that are geared towards fostering enhanced competition.

However, in much the same way that Satoshi’s resolution of the Byzantine Generals’ Problem helps to mitigate the risks associated with entrusting in third parties, blockchains also ameliorate many of the consternations associated with the competitive and exclusionary existence of prevailing concentrations of power and influence; most notably, “DeFi Legos” have come to further incentivise cooperation over competition due to the permissionless nature of smart contracts and their composability. The nature of Metcalfe’s Law (n²) gave rise to exponential growth in the value of networks such as those in telecommunications and the Internet, and when combined with blockchain it has been shown to be the most effective means for propagating the growth of a network thanks to the financial incentive that every participant can benefit from. For this reason, cryptocurrencies represent the fastest-growing technology ever to have existed, and it is forecast that there will be one billion users by 2024.

Of course, the propagation of a particular idea and the proliferation of specific networks does not happen by chance: if Bitcoin were completely useless and could not support the “store of value” narrative and entrench itself into the market by dematerialising inferior alternatives, then it would not have gained the traction and support that it has. Google Maps and SatNavs were able to dematerialise traditional and tangible maps because the digital nature of such an innovations means that they can constantly be improved, are not liable to be damaged, and are far more efficient — all of the constraints that tools and utilities may have to face in the tangible world can be circumvented by their digital alternatives. A recent example of such a societal trend would include the rise of NFTs; digital art does not require high levels of cost and bureaucracy to acquire and maintain, and the dematerialisation of the art from the physical world into the digital world transforms the industry of art into becoming more egalitarian and less elitist, since it is now open to anyone with an Internet connection.

The Rise of DAOs

In the same way that technology has improved the efficiency and meritocracy in other areas of life improving upon them in the digital sphere, so too is it coming to change the way in which we work. Decentralised Autonomous Organisations (DAOs) have recently risen to prominence and as a new way of coordinating people behind a common goal. This goal could be anything from buying the US constitution to overseeing management of DeFi platforms such as Aave, Compound and Uniswap. Undoubtedly accelerated by the incredible rise in the phenomenon of remote-working that became so dominant during lockdown, the dematerialisation of traditional office space and preexisting hierarchical structures for organising businesses is being obsoleted not only by the technological innovations that make such businesses logistically palatable, but also by changing cultural phenomena. Speaking at CoinFest 2021 in Manchester, Dominic Frisby explained his perspective on the ways in which the trend to remote work is an ever-accelerating phenomenon and that “Whilst traditional employment is not dead […] it’s on its way, and fiat currencies are limited by borders” (an issue that DAOs largely do not have to contend with). He went on to explain that the incentives for such phenomena will act as some of the most significant catalysts for those working in the blockchain space, since it is the industry that is the most predisposed to capitalise on The F.I.R.E. Movement and stands the most to benefit from more flexible working structures. Of course, one does not have to be a digital nomad to reap the rewards of such changing structures, but such organisations are particularly appealing for those who wish to leverage the opportunities of geographic arbitrage. The corollary of such decentralised organisations is that the efficiency of these communities is maximised: people all over the world are contributing to these projects 24/7 and the ability to leverage the hive-mind of collective intelligence from around the world means that traditional organisational structures are inferior by their very nature, since it is impossible for them to scale their employees and talent to the same degree, and certainly not whilst maintaining all the benefits of such flexible timetables. Those who choose to work for DAOs are not beholden to the same levels of restrictions and inevitable conformism that is inherently demanded of someone working a traditional job: there is no daily commute to work with the same group of people for the same company or organisation, and there are no exclusivity clauses in their contracts (as explained above, such a thing would not only be impossible to implement, but wholly counterproductive to the nature of cooperative innovation).

Challenges for DAOs

Nevertheless, there are inevitable challenges that DAOs face in terms of how to incentivise such contribution: many projects fall prey to a steady decline when their market caps can only be attributed to short-term speculators rather than investors and contributors whose goals align with the long-term mission of the DAO, and it is important to find ways to incentivise engagement and active contributions to help DAOs to develop and achieve their growth goals. If such progress is not adequately incentivised across the board, DAOs cannot effectively leverage the pool of knowledge-based capital at their disposal, and risk becoming “zombie” organisations whereby it becomes all too easy for stakeholders to simply enjoy a “free ride”, parasitically reaping the rewards from the contributions of those who give up their time to develop and improve upon a project. The potential for short term traders and speculators to potentially reap far larger rewards than those who believe in a project’s long term capabilities is also damaging to the core mission of a DAO, since it can play a role in disincentivising consistency amongst the community

Arguably the main problem for DAOs is the fact the lack of clarity as to what they actually are; since “DAO” has become a buzzword for Venture Capitalists working in Web 3.0, many fledgling projects have tried to capitalise on utopian ideals of decentralisation by claiming to be something that they are not. As one of the most subjective acronyms in the cryptocurrency sphere, there is a bewildering range of projects that vary in terms of their decentralisation, the extent to which they are autonomous, and even the degree to which they are organisations rather than companies or other such enterprises. The main issue with the acronym is the misleading way in which many projects attempt to depict themselves as decentralised, when the overwhelming majority are clearly not, either in terms of the concentration of native token holdings, the immutability of governance decisions, and most importantly the degree to which the community actively participates in governance. The ability for individuals to own a stake in a community and to have governance rights conferred unto them inevitably suffers from being ideologically-tainted if there are no incentives to participate — altruism to “the cause” has been shown to be an ineffective incentive time and time again, even amongst the largest and most popular blue-chip DeFi stalwarts.

A cursory examination of the governance pages for projects such as Aave and Compound demonstrates that participation in votes is almost always below 10% and with rarely more than 20 addresses participating. This is not what you would expect or hope to learn of governance tokens that have accrued market caps in the multiple billions, with further billions in TVL. Lack of community participation and ambivalence towards development is a large problem for the aforementioned, since having so few participants exposes the fact that most token holders’ incentives do not adequately align with those of the DAO; token holders often enjoy a free ride at the expense of the DAO being able to fully utilise the pool of knowledge that could otherwise be at its disposal. Without the proper incentives for people to take an active role in helping their communities rather than being apathetic or simply delegating away their potential contributions (another inherently centralising force that ambivalence causes, which is exacerbated by the fact that it means DAOs are not leveraging the full pool of intelligence at their potential disposal), the entire ethos of decentralised governance is extraordinarily flawed, sometimes in manners that are more than just misleading - many are just disingenuous. Jack Dorsey has been tweeting recently about the huge divide between VCs and their communities, and the ways in which the former often regards the latter as their exit liquidity, rather than being aligned behind longer-term goals of cooperation.

Another problem that DAOs face is that they lack the incentive to participate in the first place, since the remuneration for participation is given wholly in the native token. A DAO that cannot generate revenue, or perhaps does not have the structures in place to fully compensate their community for their efforts via fees accrued, will usually be forced to compensate their token holders (if at all) in their native token, either through yield farming, staking, or other such incentives. This is attractive for people who are bullish on the governance tokens themselves, but comes with the caveat that to redeem profits one must add to the sell pressure against the token (thus decreasing their equity in the project), which is also not a good form of alignment for DAOs. The inevitability of inflation and dilution is usually not adequately offset by distributing and sharing revenues amongst stakeholders and contributors - people are far more likely to wish that they could be paid in assets such as Bitcoin, Ether, or stablecoins, rather than embracing the opportunity cost to commit to a particular project and its volatility, amidst a plethora of less-risky investments that aren’t intrinsically dilutive, and are more efficient at aligning incentives. When such incentives are not adequately complimented by sound foundations (be it a proportional vote over the treasury, or future expected revenues - which are often highly speculative), a DAO cannot adequately scale its incentives: if too many “mercenary” yield farmers are drawn to a project solely to capitalise on the yield but sell off their rewards because they are ultimately perceived to be without value, then liquidity provision is destined to be far more uncertain and those who are providing the liquidity are thus only parasitically beneficial in the short-term.

PieDAO Solutions

Fortunately, the PieDAO community is fully aware of these shortcomings, and has thus been working to ameliorate some of these concerns and working together create new forms of governance that are more logistically palatable and desirable, with the ultimate goal of long-term alignment across the board.

Firstly, what is PieDAO? PieDAO is an asset-allocation DAO focused investing in a diversified manner for the long term. Every DAO must have an established mission as its prerequisite for success, and the ethos underpinning the PieDAO vision for long-term sustainability and the availability of automated wealth creation for the users of PieDAO’s products. For this reason, PieDAO has adopted the mascot of Ray Dalio wearing sunglasses, in a nod to the juxtaposition of hyper-flexible structures being combined with Dalio’s notorious long-term investment ethos and focus on diversification. As Harry Markowitz is famous for saying: “[when it comes to investing], diversification is the only free lunch”. PieDAO creates products that allow people to realise such goals, particularly those who believe that the the future will be bright for the digital asset space as a whole, without the high barrier to entry that would exist without it.

“Pies” are indexes created by the community that facilitate easy exposure to a variety of different assets without all the headaches that would come from actively managing a portfolio oneself. In compensation for creating and managing these products, the DAO charges streaming fees of 0.7%-1% depending on the pie and the strategies that are incorporated, such as meta-governance and optimising the underlying assets for yield. All pies start at a value of $1.

As explained on the PieDAO website, the flagship index, Balanced Crypto Pie (BCP), is:

“The most risk-minimised cryptocurrency portfolio, Balanced Crypto Pie is all you need. BCP gives equal Bitcoin, Ether, and DeFi exposure in one easy to access ERC20 token. The underlying assets in BCP are constantly taking profits and growing your holdings as it automatically rebalances to maintain the set allocation.”

The average consumer and investor has neither the time nor the desire to stay abreast of the minutiae involved in managing a sophisticated portfolio in a nascent asset class that is constantly developing and evolving. BCP offers the opportunity to investors to speculate on the industry as a whole by maintaining a balanced portfolio through the ownership of a single token: when a pie is “baked” (minted) with ETH, a smart contract will purchase the underlying tokens to ensure that the indexes are always fully collateralised. BCP holders will maintain a balanced portfolio 1/3 WBTC, 1/3 ETH and 1/3 DeFi++, which comprises a variety of blue-chip DeFi projects that have been heavily vetted by the DAO.

Everyone is catered for: even though the project is not very old, there are a variety of different pies that people can invest in: BCP, DeFi+L (DeFi large caps), DeFi+S (DeFi small caps: further down the yield curve), YPIE (Yearn Ecosystem Pie), DeFi++ (70% DeFi+L and 30% DeFi+S), USD++ (stablecoin), BTC++ (synthetic BTC), and PLAY (an index focused on gaming, NFTs and the Metaverse, made in collaboration with NFTX). Although the initial composition was revised in PIP-59, this project has been emblematic in capitalising on the growing popularity of play-to-earn games such as Axie Infinity, Decentraland, and The Sandbox, and served to show the capability of DAOs when they collaborate with one another.

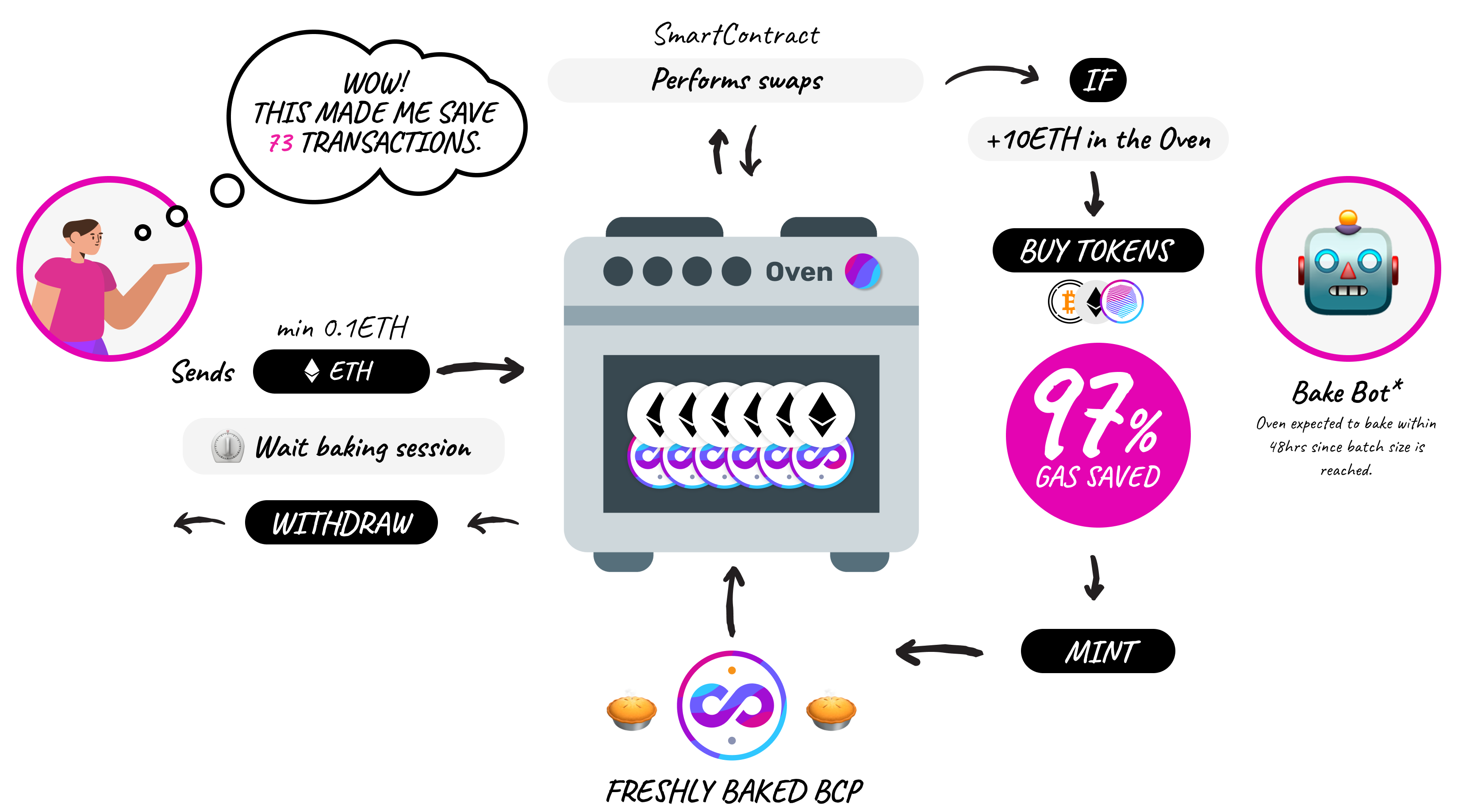

To acquire pies one can choose to buy pies directly from the market. The flexibility of “DeFi Legos” has resulted in liquidity pools being spread across SushiSwap, UniSwap and Balancer, depending on what the community deemed most appropriate; however, users of PieDAO products do not need to be concerned with this, since PieDAO has a built-in exchange that allows for seamless trading between their products with optimally-low slippage. Alternatively, pies can be “baked” in The Oven, in order to save gas fees. Anyone can deposit ETH into the oven of whichever particular pie is is that they want to buy (PLAY, for example), and when there is at least 10 ETH in The Oven and gas prices have fallen below 100 gwei, The Oven will bake and buy the underlying assets. The ingeniousness of this particular onramp to the ecosystem is that the gas fees are shared by the various parties that have contributed ETH, thus resulting in a large saving in terms of fees.

Being so focused on indexes has a huge advantage in terms of short-term flexibility, as well as being able to leverage all the opportunities that abound in DeFi: in The Exponential Age, those projects that are the most well-placed to capitalise on network effects are the ones that will accumulate significant amounts of capital, whether it be intellectual or financial. Cooperation between DAOs is common, and this allows ideas and improvements to scale much more rapidly than with traditional organisational structures: competition becomes naturally obsolesced by the free market as it becomes abundantly clear that improvements to one project may benefit others - the result being that market inefficiencies in DeFi can be closed very quickly, and good ideas can scale to reach their maximum potential just as quickly.

Such a project inevitably requires a lot of liquidity to scale, particularly to ensure that the indexes stay as close as possible to the underlying NAVs. For this reason, PieDAO embarked upon a The DOUGHpamine Incentives Programme. Anyone can either stake their BCP, or stake their LP tokens to farm the native governance token (DOUGH), at very impressive APYs: current rewards for the staked SushiSwap DOUGH/ETH LP stand at around 200% per annum. Of course, this may immediately strike some as unsustainable over the long term, and only time will tell, but the community has taken some steps to encourage cooperation toe ensure the longevity and efficacy of the programme. Firstly, only 20% of farmed rewards are instantly redeemable, whilst the other 80% is gradually released after the one year vesting period. This dramatically reduces sell pressure and means that community is able to sustainably incentivise liquidity provision.

Nevertheless, this programme was not complete: after the vesting period one would quite naturally expect the selling pressure to increase dramatically, and the expectation of this on behalf of liquidity providers would be to withdraw liquidity, thus exacerbating the issue further. This is where most DAOs and most open source projects have failed: a lack of continuous incentive to be able to sustainably ensure that the DOUGH can at least bootstrap itself to a significant size without taking huge risks and making large trade-offs for sustainability in the long term. Fortunately, the ideas conceived in early August and subsequently executed in PIP-60 have fixed this issue, and come to function as the “missing piece” of DeFi.

The Governance Revolution

The aforementioned challenges that DeFi governance (and therefore DeFi itself) currently faces are largely due to, or result in, some level at which incentives are not perfectly aligned. The ramifications for having so many disparate incentives can be destructive for DAOs (the most notorious example of this being The DAO, which resulted in Ethereum Classic), since lack of incentive alignment obfuscates what the mission of the organisation really is, and why a community is necessary in the first place - communities can also be torn apart by a lack of focus on specific objectives and why they are necessary. This is exacerbated by the fact that DAOs in their current form are quite weak, due to the mercenary nature of “The Wild West of DeFi”: loyalty is hard to come by, and often isn’t satisfactorily reflection in remuneration.

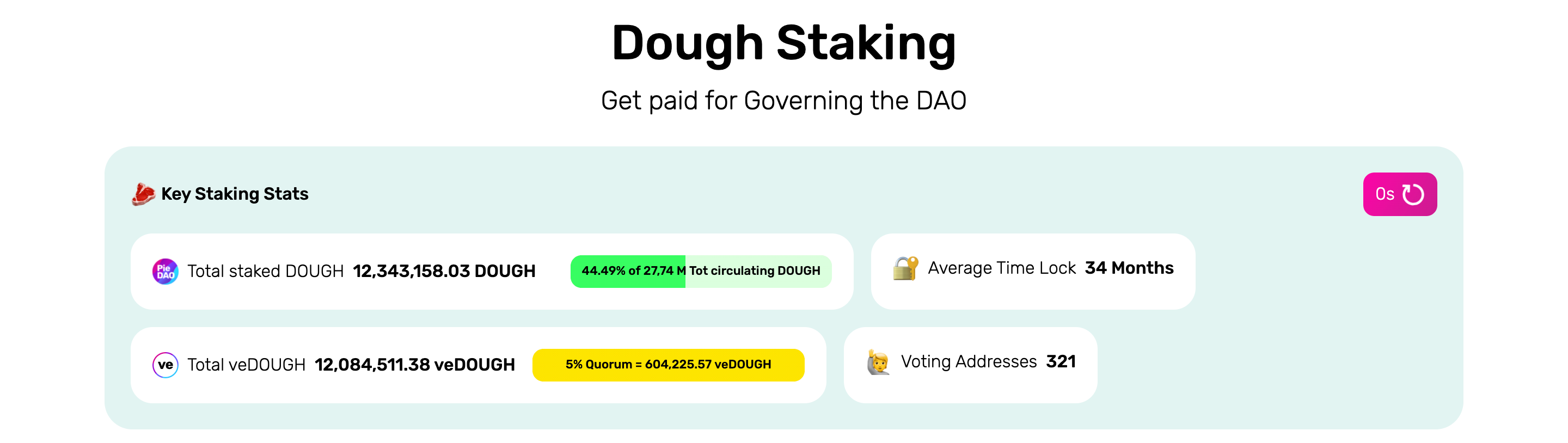

PieDAO’s governance model depends on a programme of “governance mining”, whereby those who actively contribute to PieDAO by participating in governance proposals are rewarded via revenue that the DAO generates. Holders of DOUGH can choose to stake their tokens in exchange for Vote Escrowed DOUGH (veDOUGH) for a period between 6 and 36 months. Assuming that they participate in voting on Snapshot, they will be eligible to claim SLICE in the first week of every month. SLICE represents one’s share of revenue generated by from fees on pies and farmed treasury assets, and the rewards to be added to its components are voted on monthly.

VeDOUGH also alleviates the potential sell pressure from farmed Escrowed DOUGH (eDOUGH), since PIP-67 established the creation of an eDOUGH to veDOUGH bridge. This means that eDOUGH can still either be redeemed for DOUGH after one year, but after just six months one is eligible to bridge their eDOUGH to veDOUGH and participate in governance (thus earning more rewards).

Bearing in mind the total market cap of circulating DOUGH sits at just under $7m (fully diluted $42m) and the TVL for PieDAO products stands at around $13m, the current incentives for staking DOUGH for veDOUGH (given that just under 50% of DOUGH is staked for veDOUGH) can be quite profitable. The monthly treasury reports demonstrate how the treasury, which currently stands at a value of over $16m, has been extraordinarily successful in managing the accumulated funds, and been employing profitable tactics such as yield farming, staking, and leveraging ETH.

One of the popular critiques of DAOs is that they are unable to scale: amongst the older generations it is a particularly popular notion that people cannot simply work as effectively remotely as they can in an office, and people will never be to organise themselves effectively. Even sharing DAO revenue with active participants is not often enough to achieve success in all specialised areas: why would someone put hours in writing Solidity when their remuneration is proportionally the same as anyone who is a stakeholder? This question has meant that remote organisations have come to form working groups, in which individuals who have built their reputation come to lend their expertise in whichever way is required. They could be treasury management experts, programmers, evangelists, or hosts for PieDAO events. The KPI options developed by UMA have meant that it is possible to stipulate with smart contracts that rewards be distrbiuted to particular contributors (or to incentivise members of the DAO to behave in a certain way, such as rewards distribution upon reaching certain metrics), or to a particular committee, contingent on the extent of their future success.

Hence, by aligning the incentives of those who share long-term goals, PieDAO has been able to unite its community behind shared incentives and common goals, and is growing rapidly due to the high levels of remuneration for those who participate. Last month, the second ever distribution of SLICE ($400,000) was distributed proportionally between the 229 eligible wallets - already this month the number has grown to 321 hodlers of veDOUGH.

Closing Thoughts

It is my contention that this revolution of aligned incentives through such governance structures for the means of fomenting a wealth creation community is a brilliant “missing piece” of DeFi.

Firstly, the long-term vision of investing via diversification is perhaps too significant to overstate, and the mission to make such tools available to anyone with an Internet connection is a noble endeavour.

Secondly, the fact that the governance structure rewards contributors represents a clear example of the dematerialisation of traditional asset managers. Organisations such as PieDAO are not beholden to a lot of the inefficiencies that prevail in the current space of “traditional finance”. They are more flexible, have access to more information, are at the forefront of a technology revolution, and are developing with long-term consumer facing products in mind. By very virtue of being on a blockchain and organising through Discord, I would contend that DAOs are not only more scalable, but that the people who work for them are happier, and thus more productive. In an era in which personal freedoms and liberties are being eroded to the benefit of totalitarian health regimes around the world, the state under fiat continues to grow larger and occupy more of a say over our lives. Being part of a DAO such as this is not only a rewarding community to be a part of, but it is an example of capitalism's necessary competitive antithesis to expanding government power, in a way that simply wouldn’t be feasible were it not for DAOs - people can work for DAOs regardless of the situation in their home countries; as long as they have an Internet connection to contribute their remuneration is secure.

Lastly, the Cambrian explosion of innovation that has resulted from finding a way to perfectly align incentives with veDOUGH is difficult to overstate: PieDAO has engineered a way to solve the “free riding” problem of DeFi governance participation, and this is reflected in the statistics: the double-digit level of wallet participation across DeFi blue chips such as Aave and Compound (the former with 103,000 holders and the latter with 185,000) compared to the 82.3% participation rate of PieDAO demonstrates that this model works. It is no surprise that success comes to projects who are able to fully align an enthusiastic community behind a noble goal. Some of these projects being worked on by various members of the community include working with Winterbears on establishing a future index for NFTs, as well as a $SCALE pie focused on creating an index for projects associated with Ethereum scaling solutions. If you would like to participate in any way then feel free to join the Discord and get involved. Anyone is free to claim bounties to help the DAO in any way they can.

Useful links for PieDAO:

Website: https://www.piedao.org/

Discord: https://discord.com/invite/SDnudcu

This is an excellent exposition of the current state of affairs both for DAO's generally and PieDAO specifically. I do agree that team members at PieDAO have found ways to incentivize the goals of investors with the long term goals of PieDAO. I for one, believe in the ethos and values of this organization. You don't need to be a big timer or a whale to benefit. Since joining the group I have personally watched the growth and maturation of this DAO. Even small time investors can contribute to the overall success of the community. Come check us out and see what you think.

Hello sir/mam

how are you?

i need guest paid guest post on your site https://www.business2community.com/

tell me price do-follow link and permanent post

i am waiting your good response

thanks